Home Lending

I helped an investment firm’s private banking arm become a competitive home lender

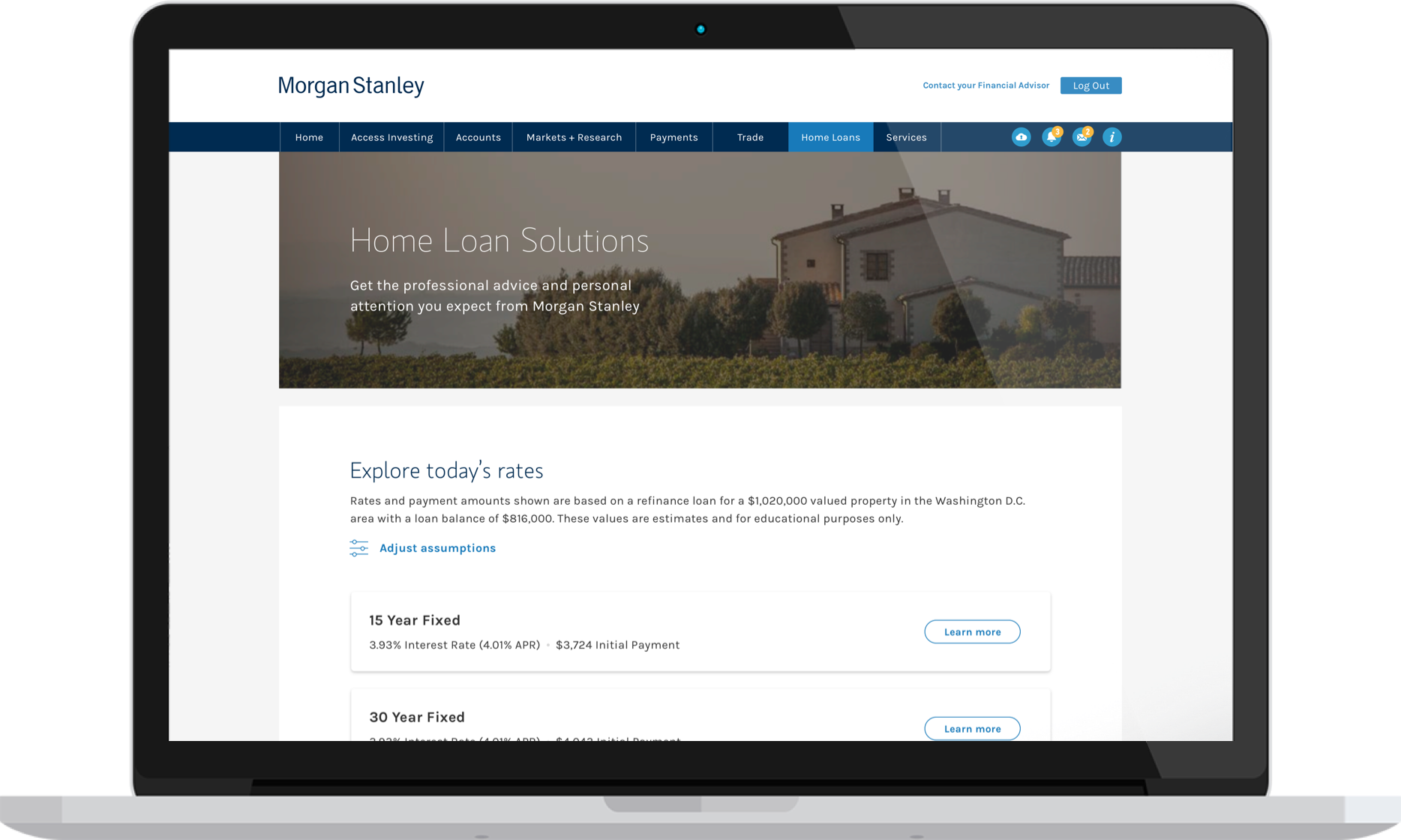

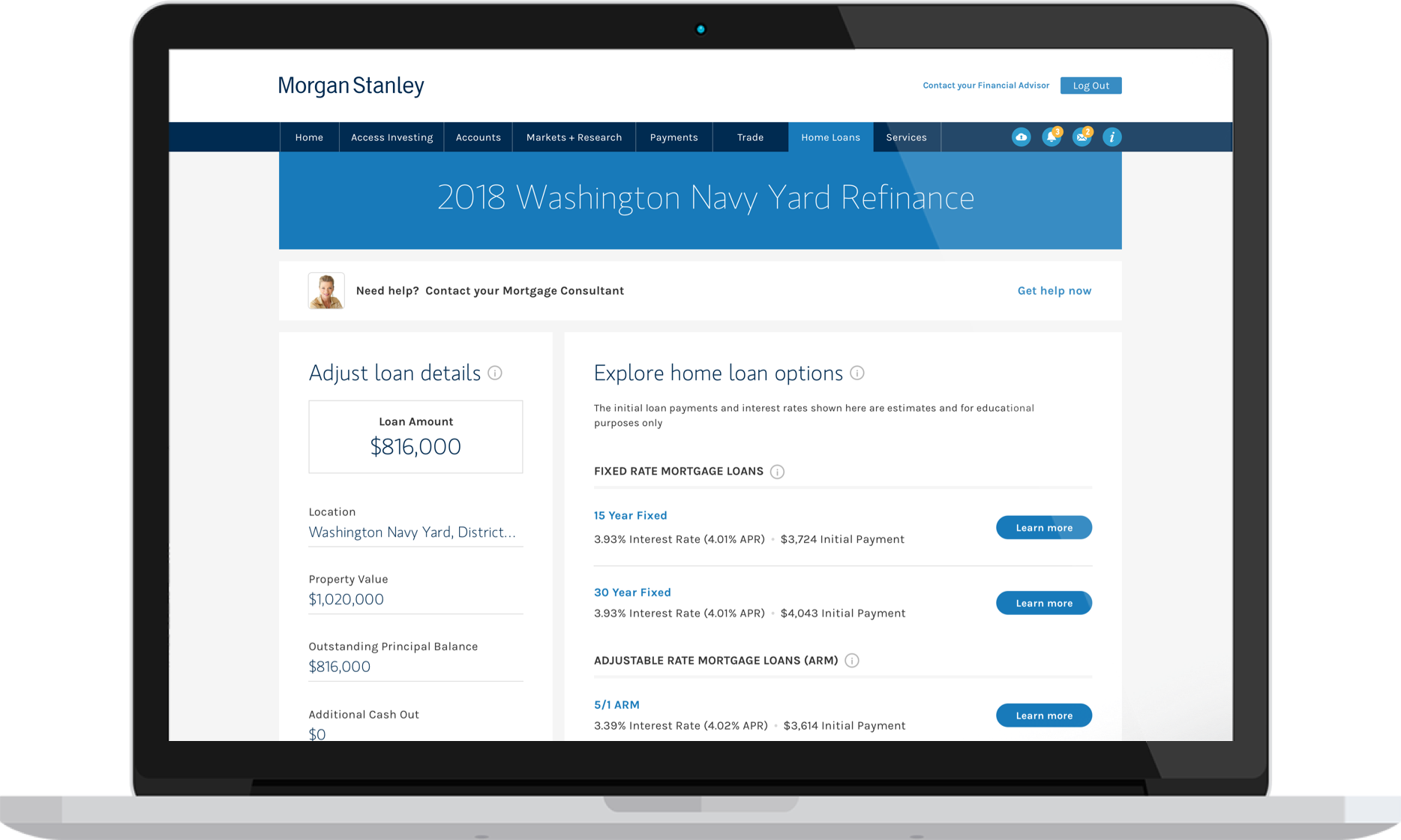

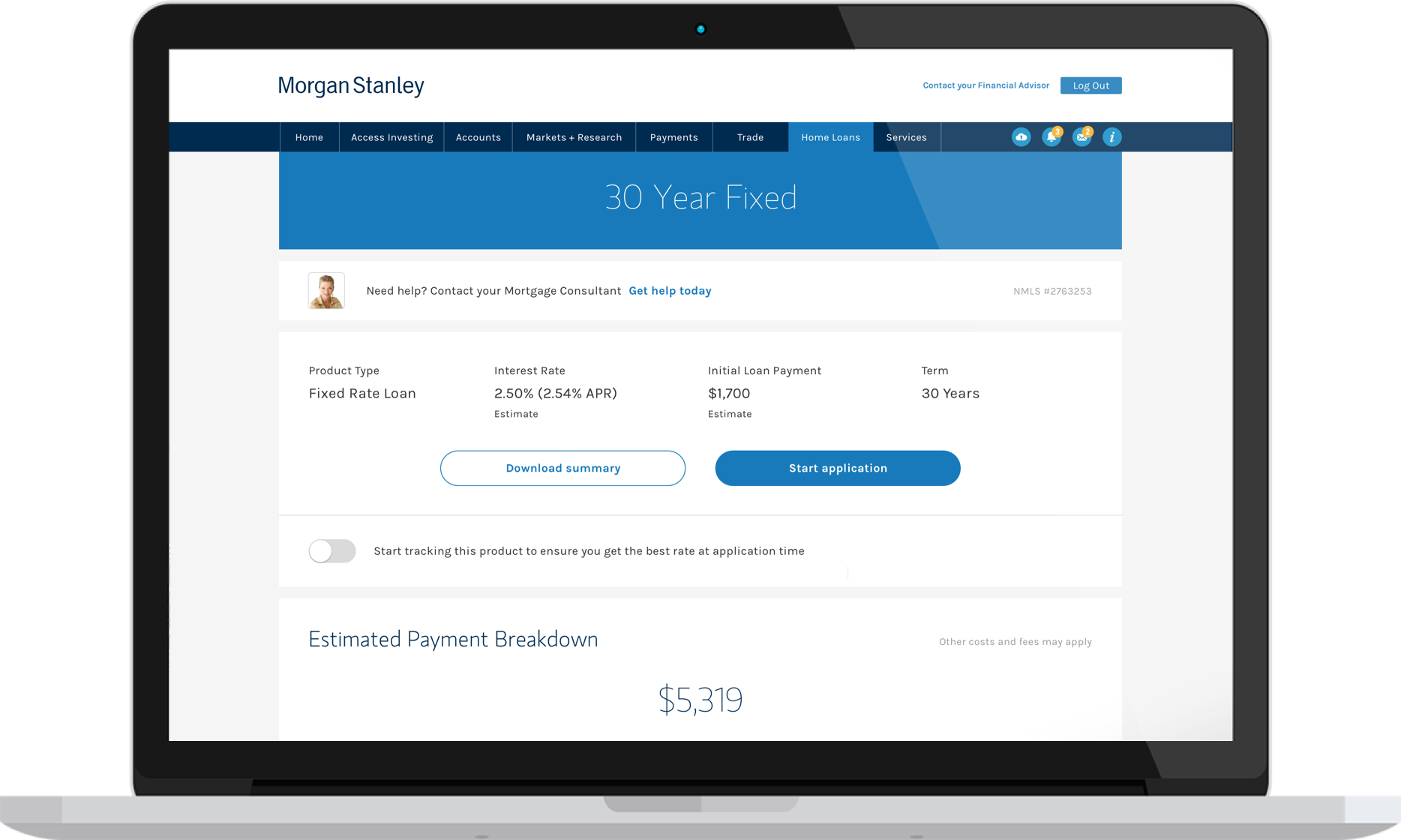

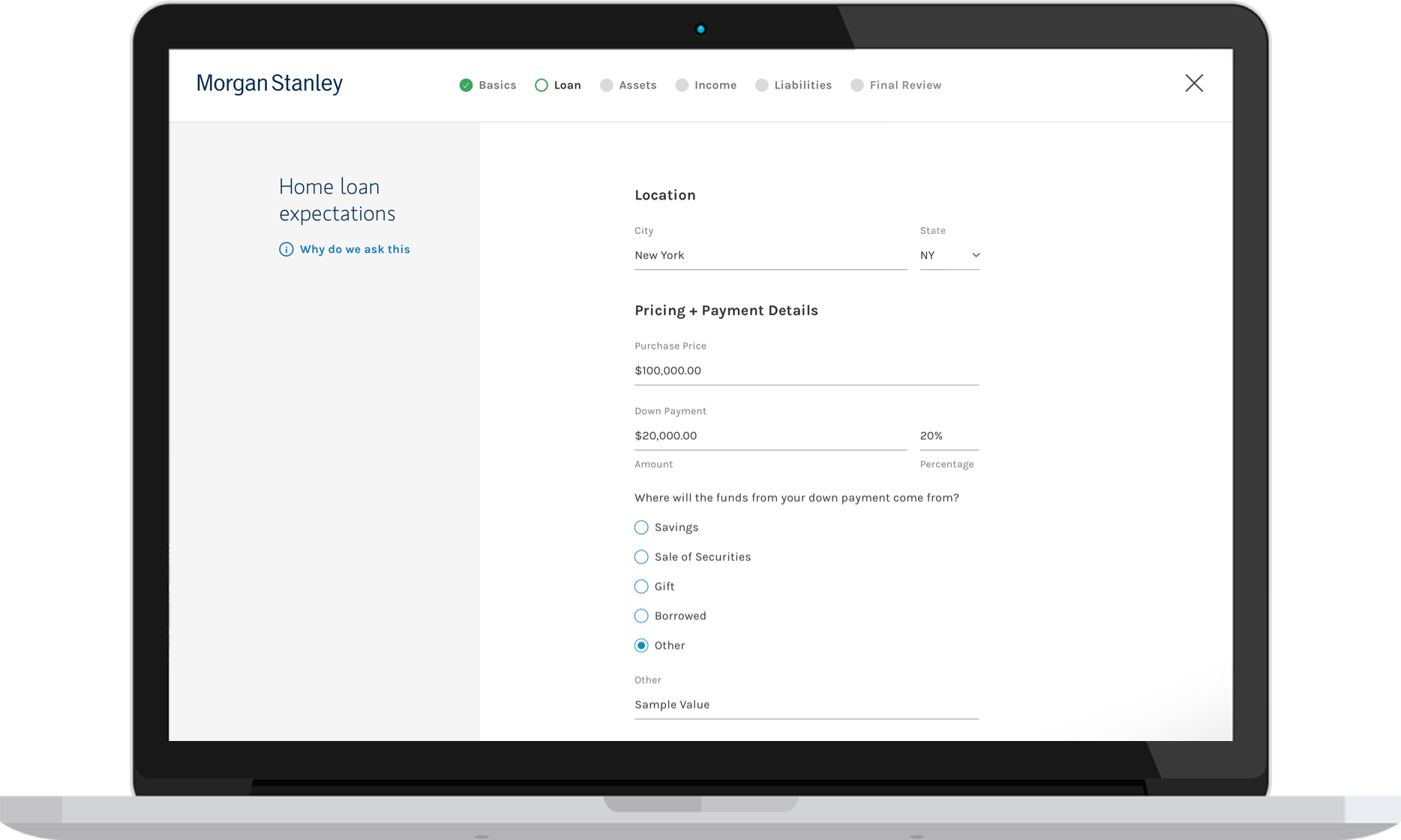

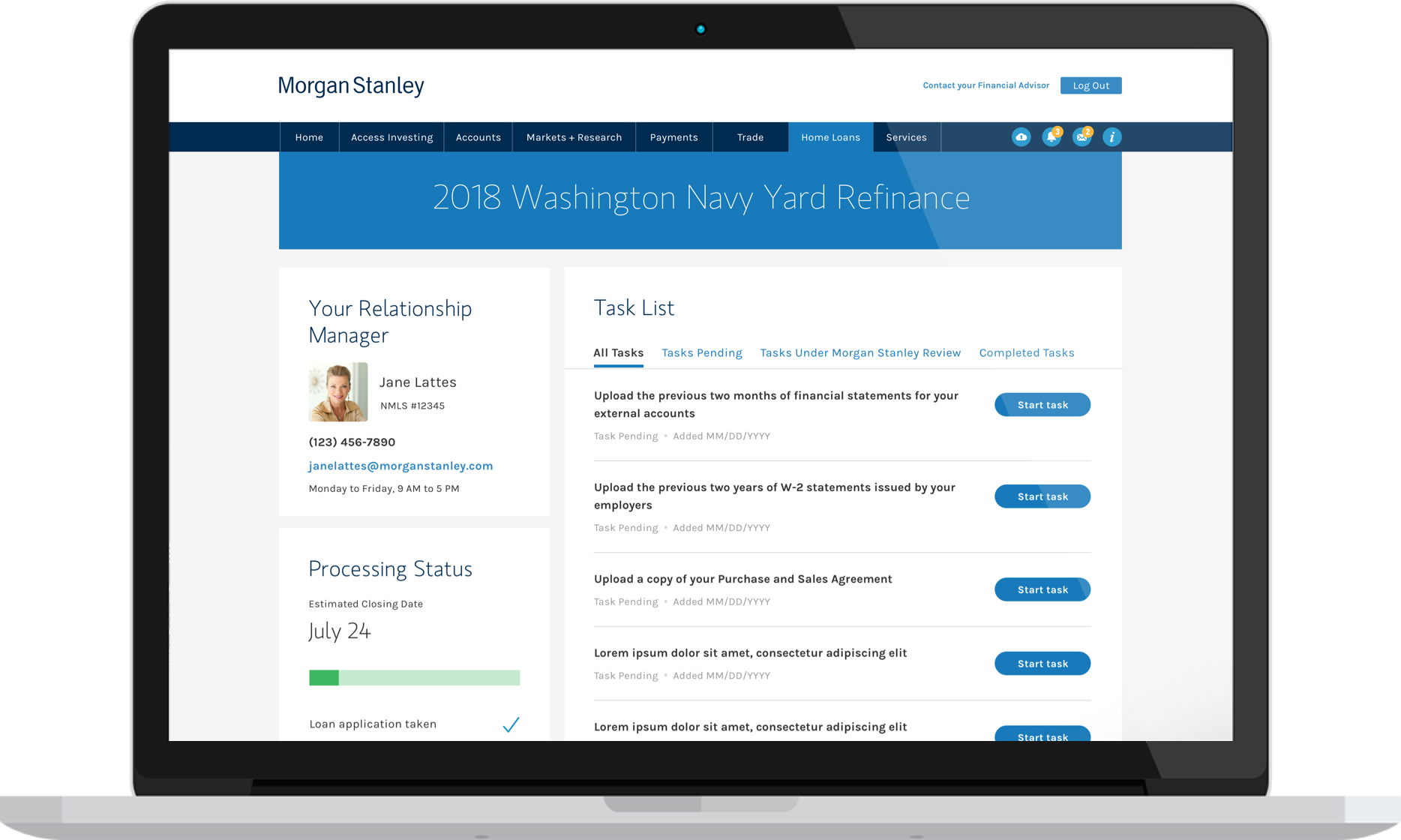

Home Loans encapsulated the Firm’s digital strategy to become a major home lending competitor. At this time, the product offering included:

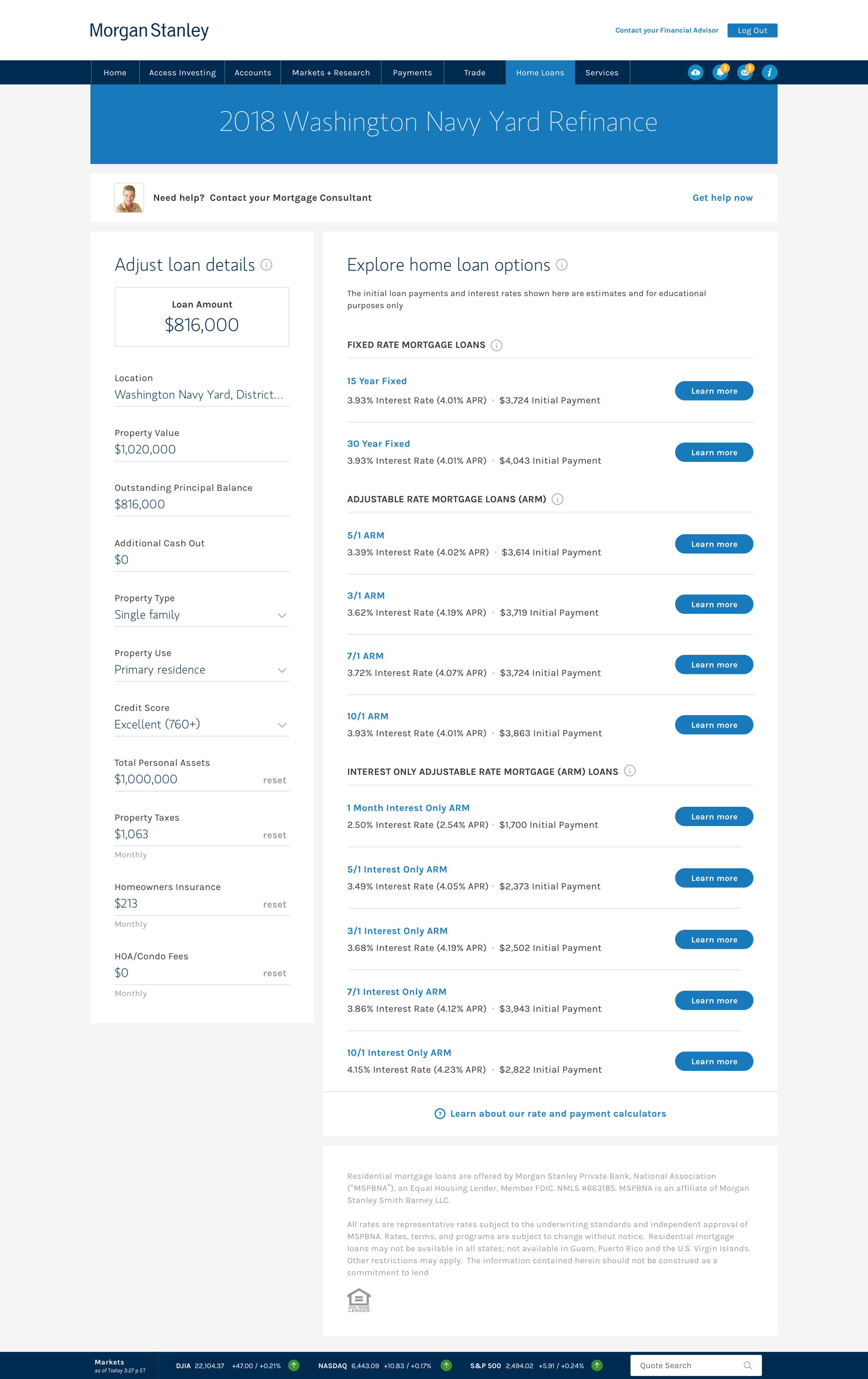

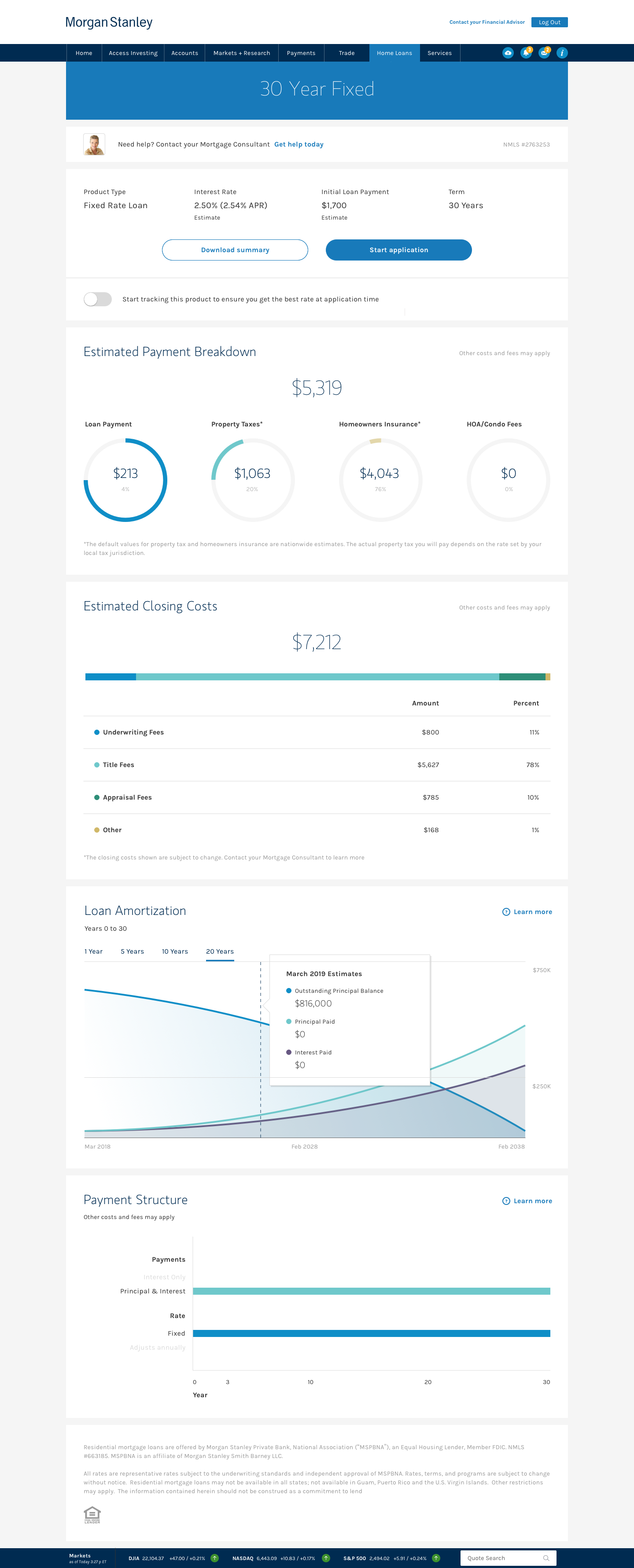

A mortgage calculator for product rates, amortization, and other key lending details;

The mortgage application, also known as the 1003, for originating the loan;

A document management tool to facilitate underwriting & processing to verify eligibility for credit

Over the course of 8 months, alongside the Private Banking Design Lead, we strategized, designed, and delivered the shopping and origination journeys, closing out this major lending product’s first phase

The beginning

My first task was to build out the mortgage calculator experience. Design deliverables were developed and socialized over an 8-week period, with weekly reviews with our Product and Technology stakeholders and a user research sprint to assess general usability and the value proposition

Simultaneously, we interviewed key Sales team members and completed empathy mapping exercises to create a "working" customer journey. This artifact helped better empathize with our clients as they go through the mortgage process and anticipate their needs

The setback

In the long run, it benefitted all the teams and we became a stronger triad

When it was time to develop the mortgage application experience, Product, Technology, and Design failed to hone in on specific use cases, and underestimated the level of effort required for such a large scope. The timelines quickly became too aggressive and unrealistic

When it became evident that we weren’t going to meet these deadlines, we pushed back against Product and Technology and produced a more realistic timeline, a more defined scope, and a chance to take on the work in a more strategic manner rather than reacting and issuing a potentially sub-par experience

Admittedly, it was a very hard conversation to have, but in the long run, it benefitted all the teams and we became a stronger triad

How we recovered

We focused on refinance loans for existing clients

We agreed to limit our scope to a joint refinance application between spouses based on client engagement strategy for the initial pilot.

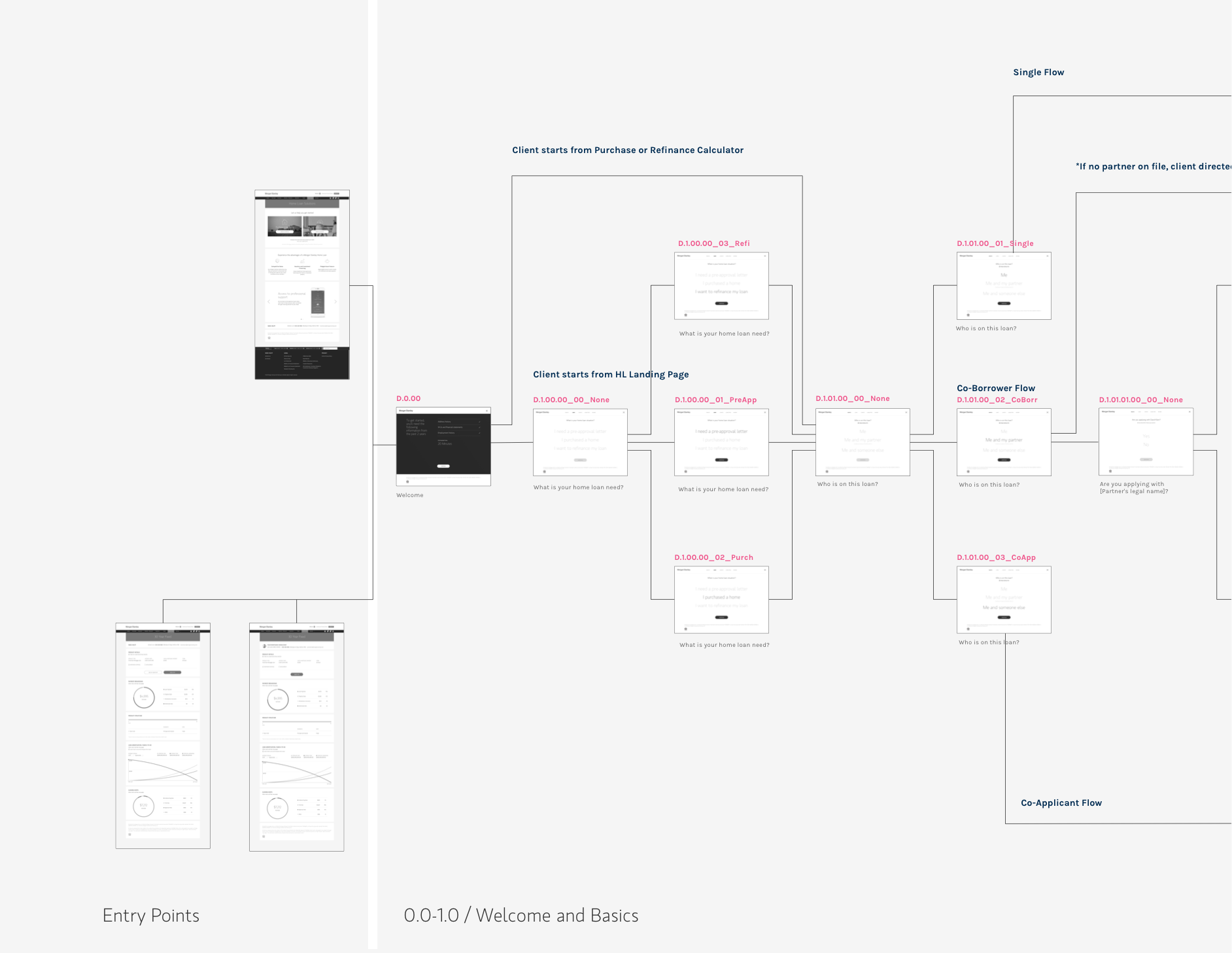

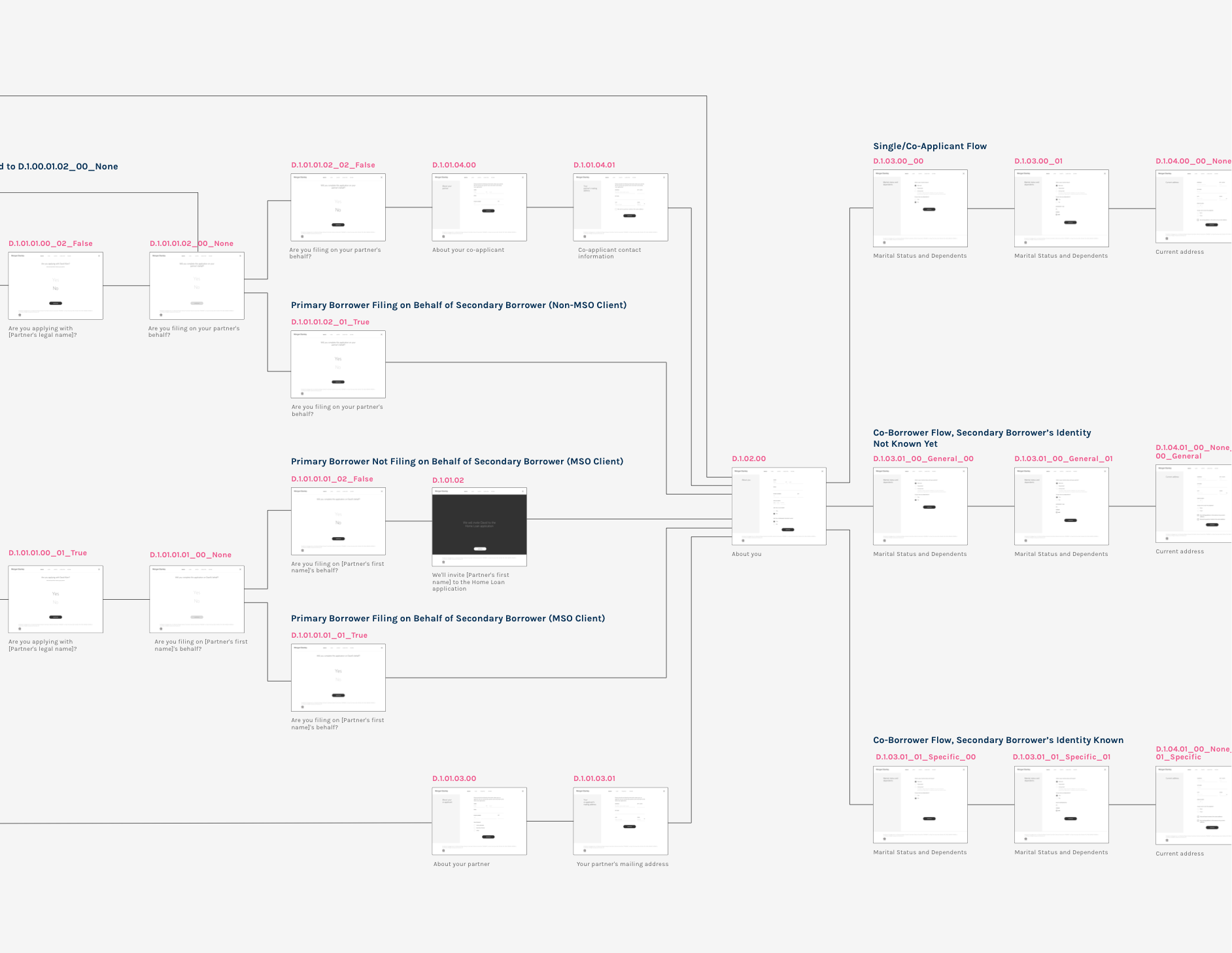

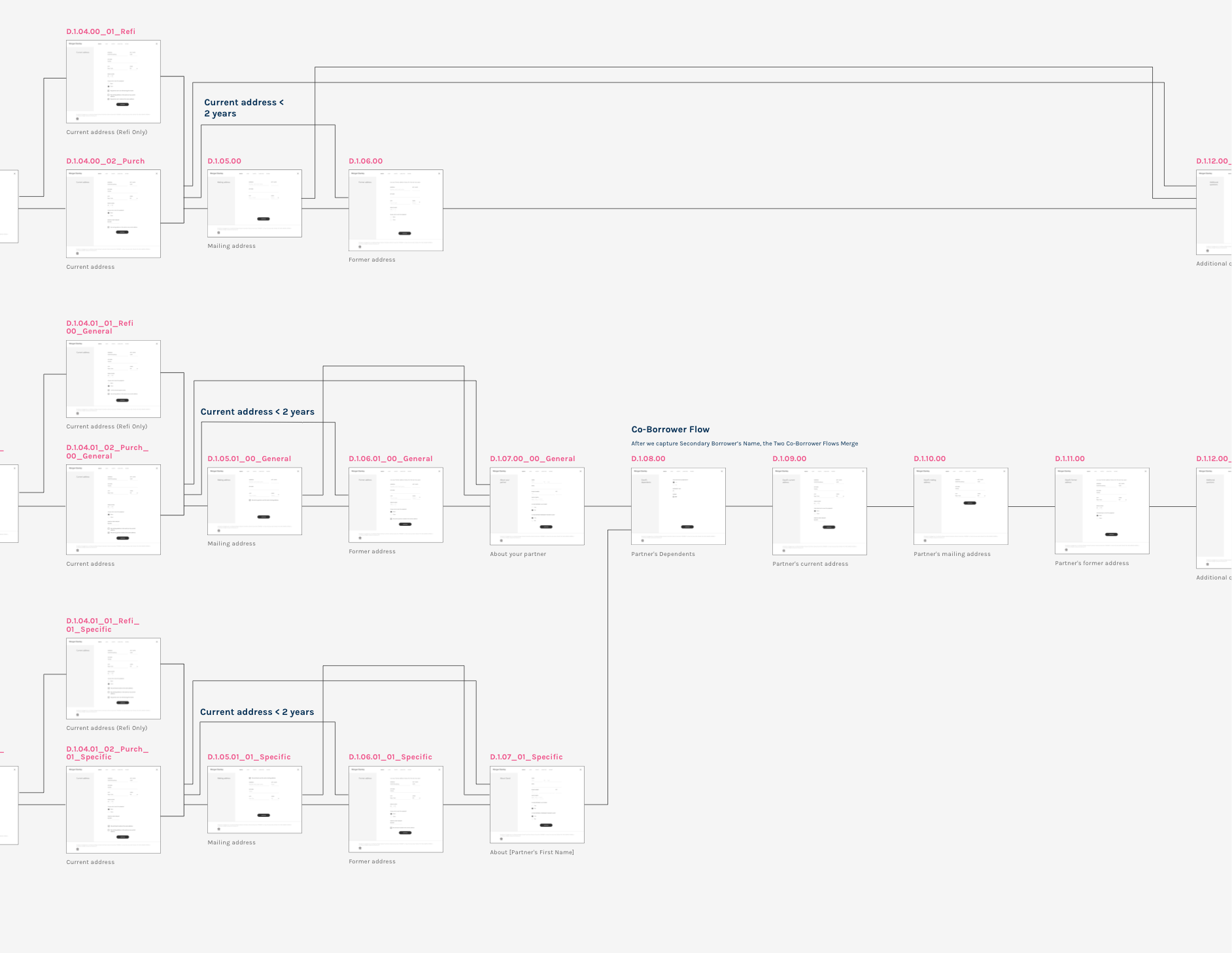

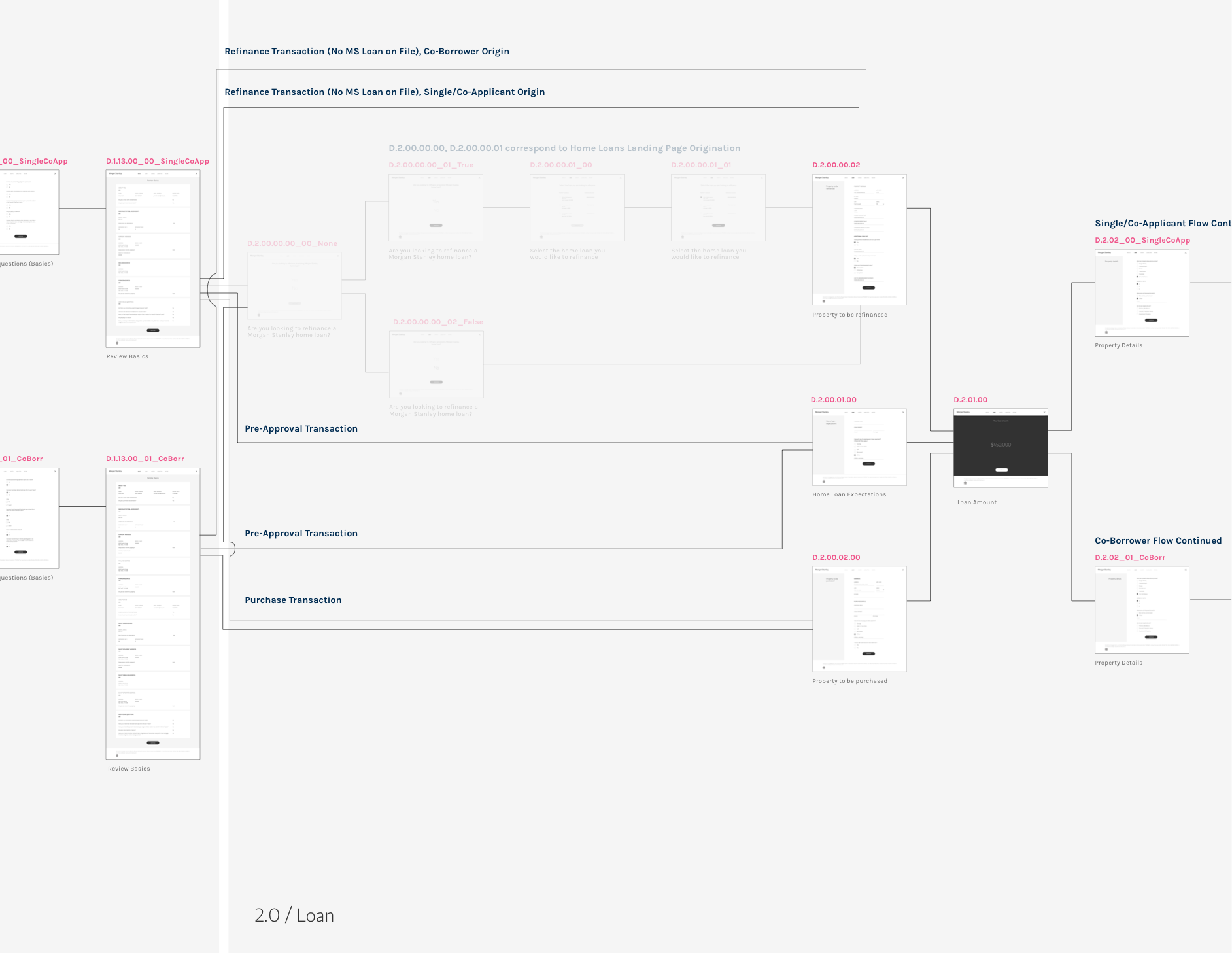

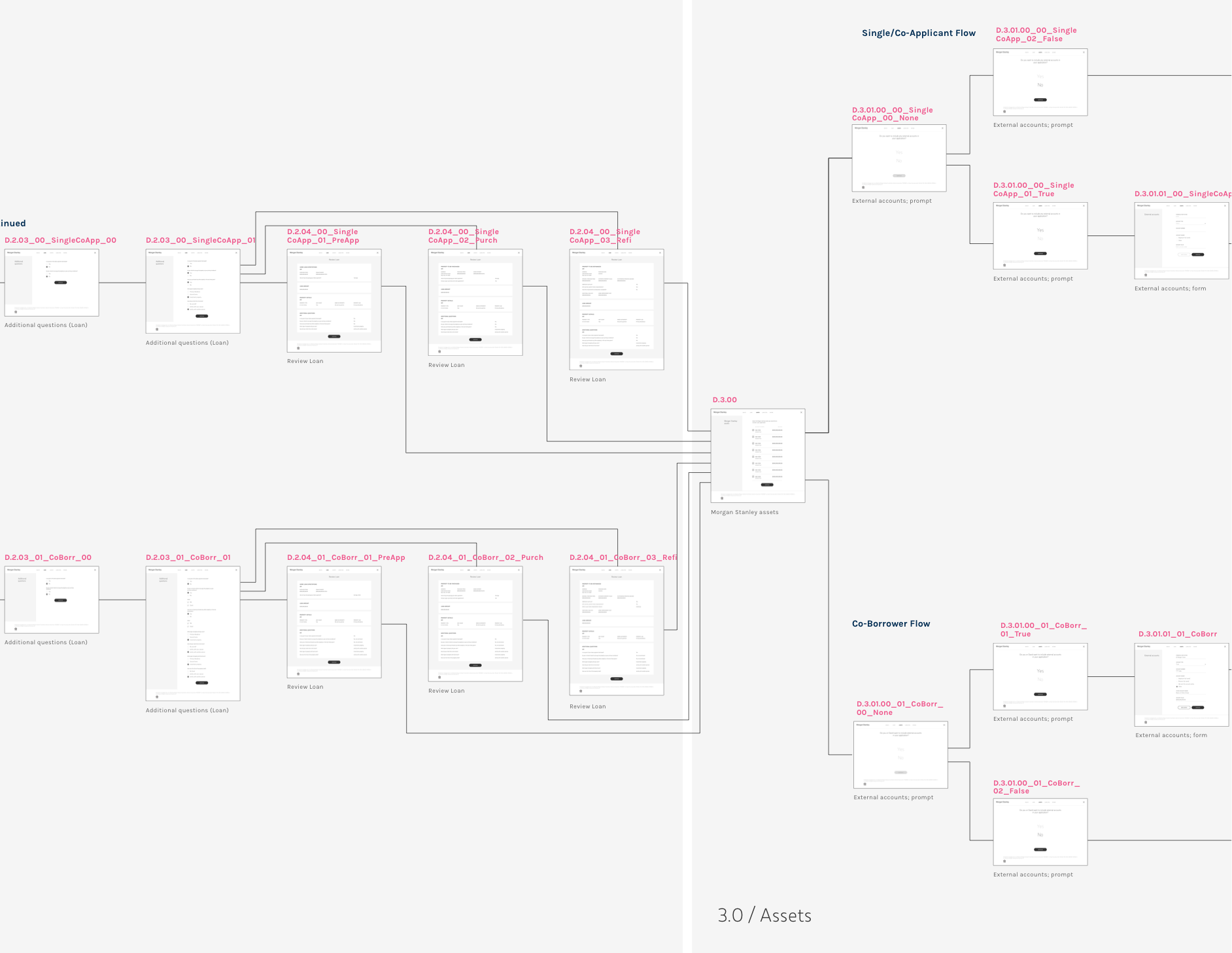

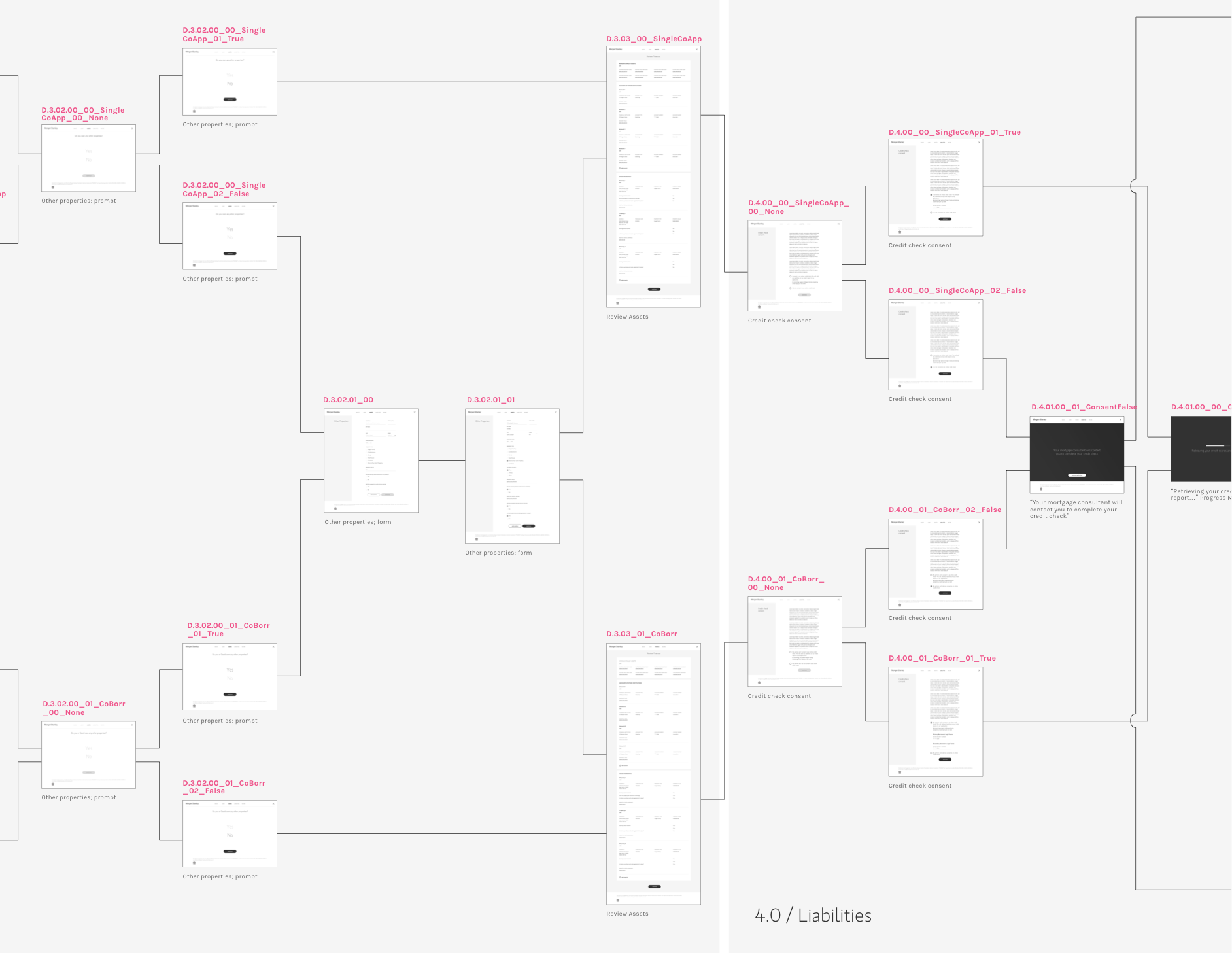

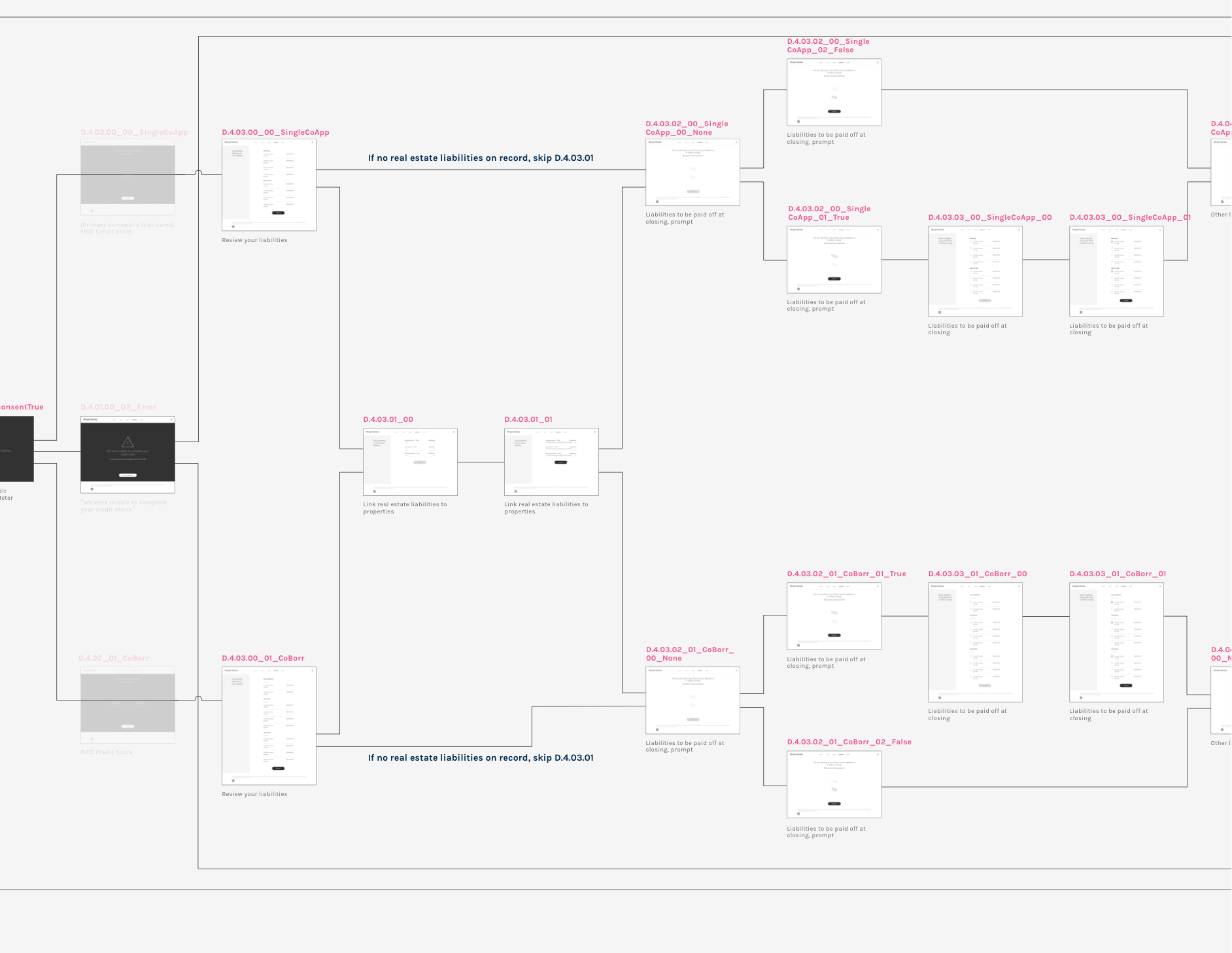

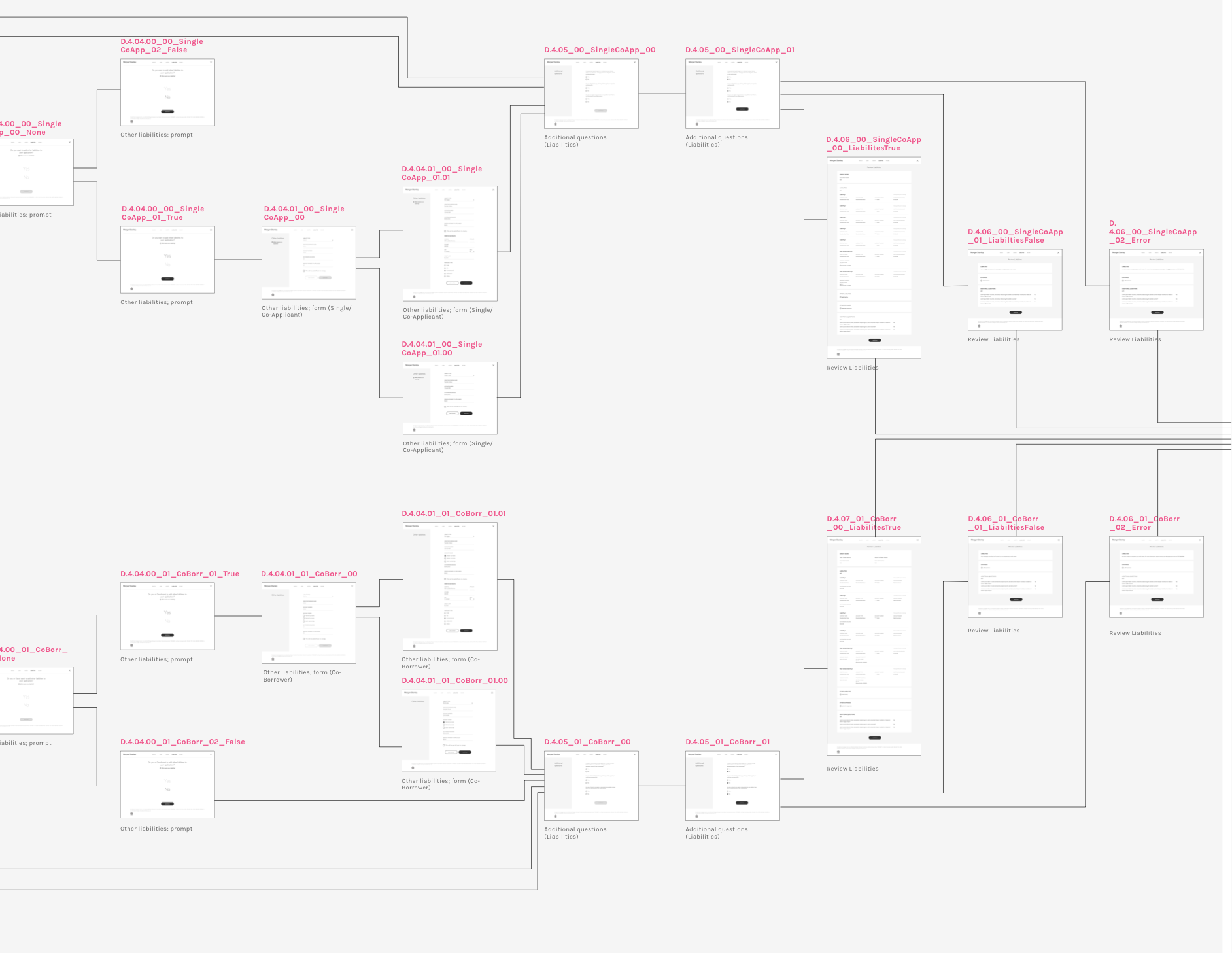

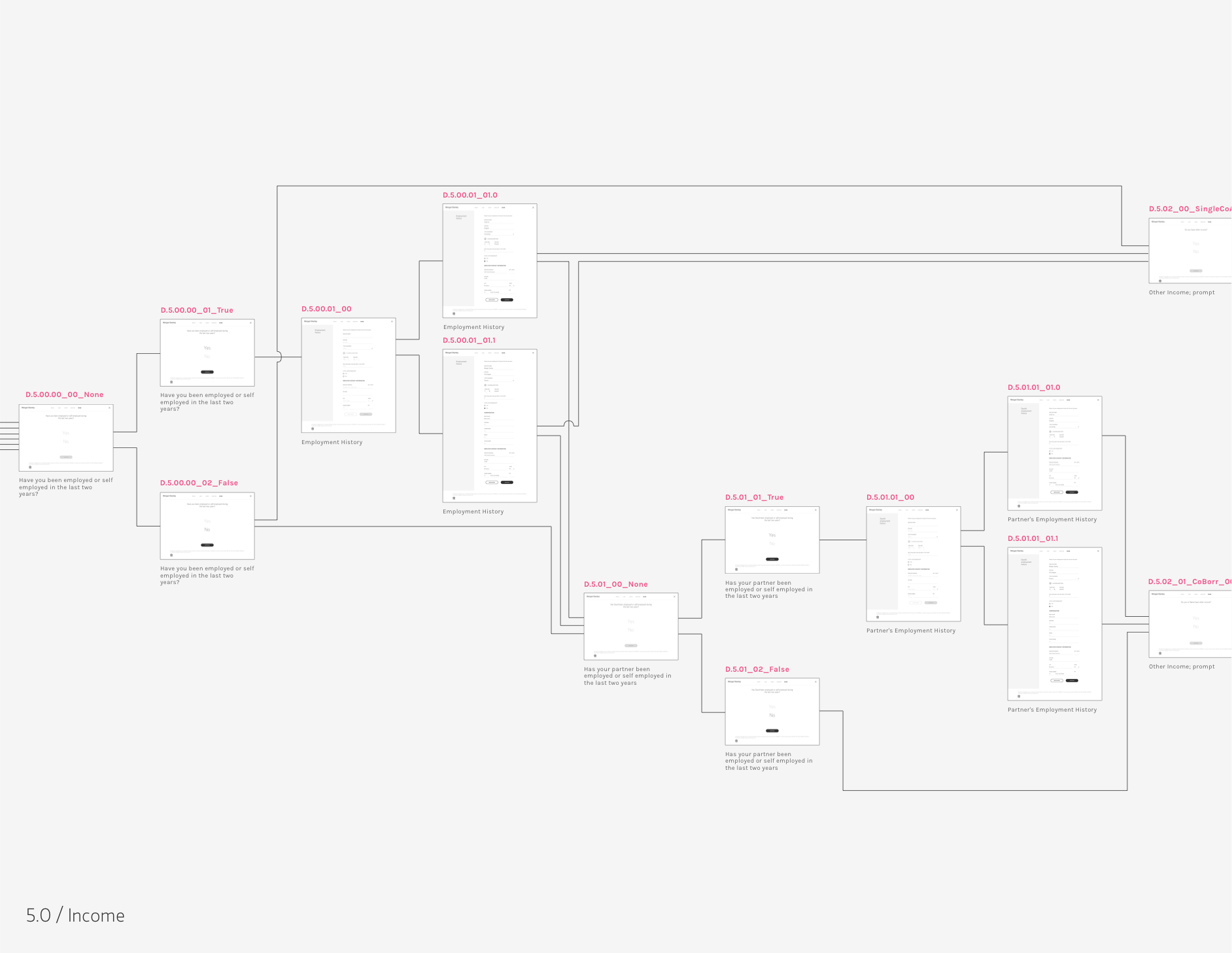

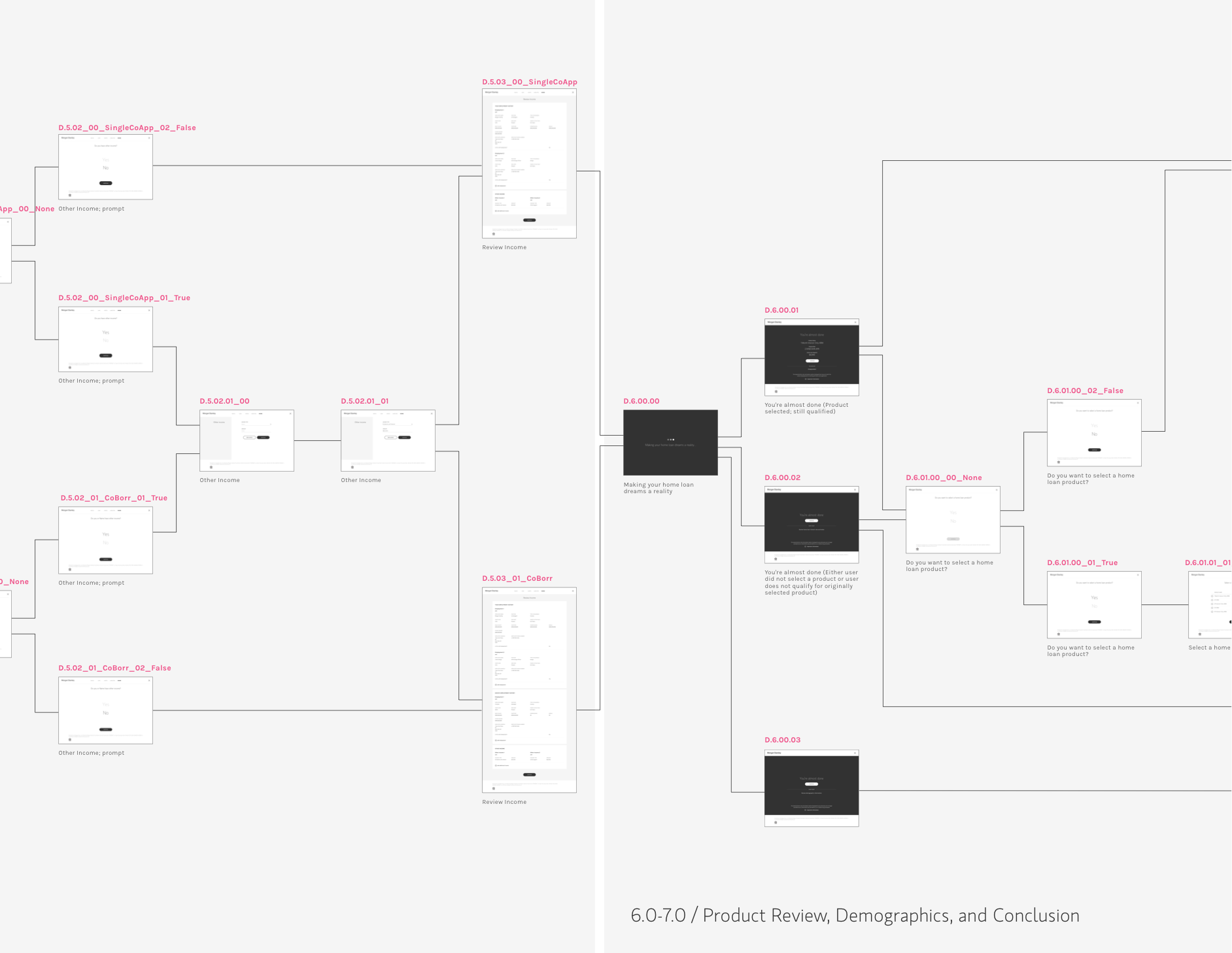

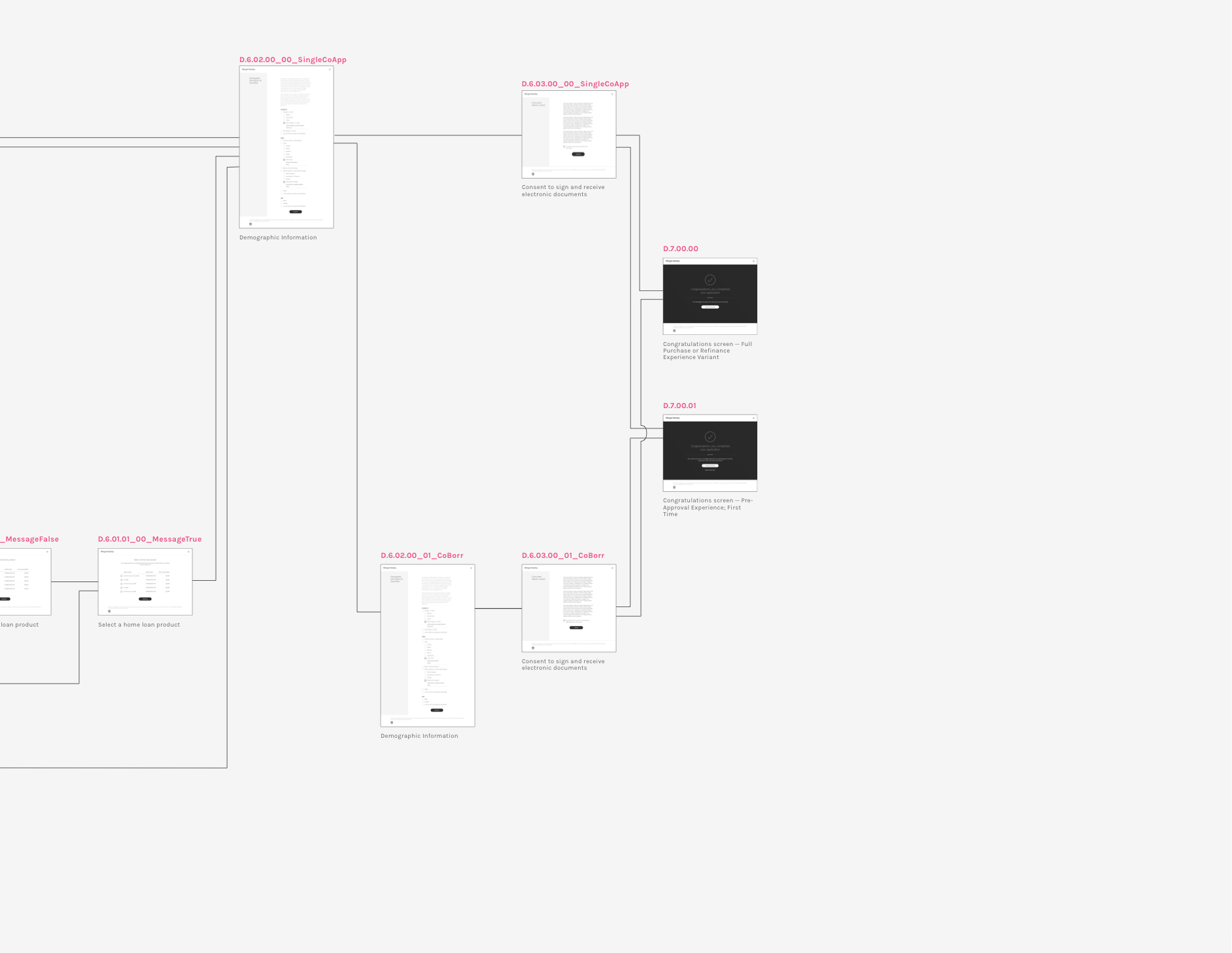

We produced an end-to-end user flow

We mapped out and organized the loan application’s required fields. This informed a set of low-fidelity wireframes that were then tied together in a comprehensive end-to-end user flow.

This artifact became a “source of truth” for developers, designers, and product owners alike over the course of development

We prepared for user research with real clients

We shifted gears and engaged Market Research and our User Research partners to validate the value proposition of our mortgage calculator and application experiences

We issued a desktop prototype that was then used for remote user testing, which took place over the course of 2 weeks with clients in our Mid-Atlantic and West Coast branches

Key research findings

Overall, users responded positively to the mortgage application experience and successfully went through flow quickly despite its length

Minor adjustments based on the client mental model

There was feedback around the placement of “Income” within the overall flow: users expected to disclose their income soon after their assets, revealing a gap between the user mental model and the tool’s sequencing

Offer contextual help & support

There was also feedback around the content and users wanted help and documentation to understand specific terms

Highlights from Pilot Launch and beyond

November 2018

The mortgage calculator and application are successfully piloting with employees and select clients across the United States. Reduced client service center calls are already being observed as a result of this self-service addition to the Morgan Stanley product suite

February 2019

Mortgage application experience expands to more markets. Applications become entirely self-service and loans exceeding $2.5 million are issued within the first week

January 2020

The Firm’s 4Q19 report communicates Wealth Management’s “higher average rates and growth in bank lending”